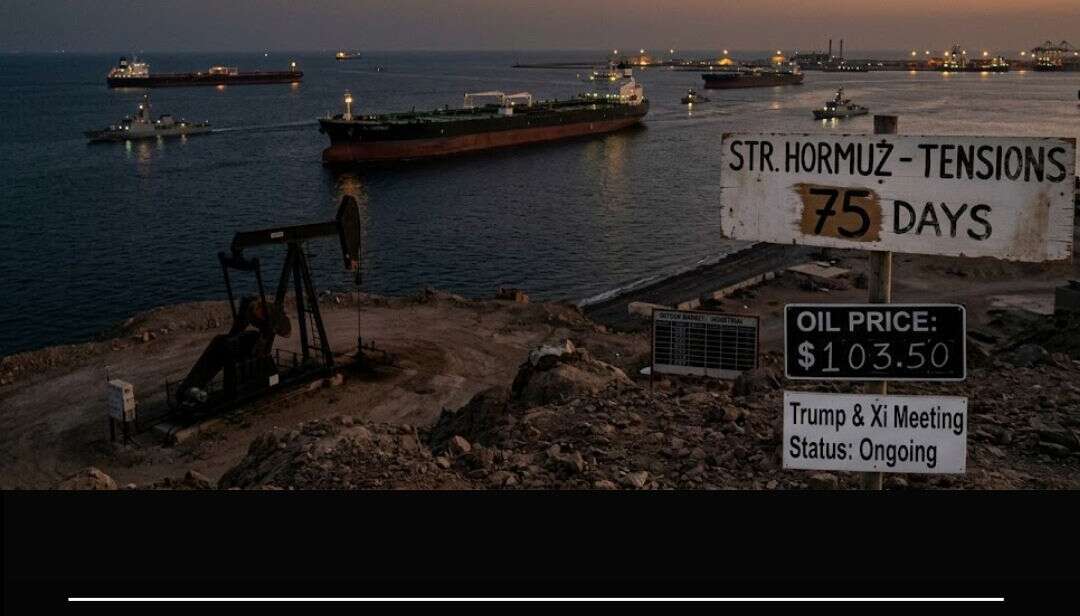

Seventy-five days after the most consequential closure of the world’s most important oil chokepoint, the numbers remain brutal. Oil above $100. Ship transits down 95%. Global inventories depleting at a record pace. And in Beijing, the two leaders who may hold the only real key to ending it are sitting across from each other for

Seventy-five days after the most consequential closure of the world’s most important oil chokepoint, the numbers remain brutal. Oil above $100. Ship transits down 95%. Global inventories depleting at a record pace. And in Beijing, the two leaders who may hold the only real key to ending it are sitting across from each other for the very first time.

On May 14, 2026 — Day 75 of the 2026 Strait of Hormuz crisis — Brent crude traded at approximately $105 per barrel and West Texas Intermediate sat just above $101, with both benchmarks holding the triple-digit territory they have occupied almost continuously since late March. The numbers represent a 45% surge from pre-war levels of around $72 per barrel, a price shock the International Energy Agency has formally declared the “largest supply disruption in the history of the global oil market.”

That record was set in the narrow, 21-mile-wide corridor between Iran and Oman — and it shows no sign of being broken in the right direction anytime soon.

What 75 Days of Closure Has Done to the World

The scale of the disruption is difficult to comprehend in conventional energy market terms, because it has no modern precedent.

Before the Israel-Iran war began on February 28, 2026, approximately 25% of the world’s seaborne oil trade and 20% of global LNG passed through the Strait of Hormuz daily — roughly 130 ship transits per day. By March, that figure had collapsed to just 6 transits per day — a 95% decline in less than two weeks.

The US Iran war has created a dual blockade: Iran closed the strait to non-Iranian vessels on March 4, and the United States imposed a naval blockade on Iranian ports from April 13. The result is a chokepoint frozen in both directions, with over 800 commercial vessels and an estimated 20,000 seafarers still stranded inside the Persian Gulf.

OPEC’s collective production has fallen by more than 9.7 million barrels per day since the war began — a drop of over 30% from pre-war output. Kuwait, Iraq, Saudi Arabia, and the UAE collectively saw production fall by at least 10 million barrels per day by mid-March as land and sea logistics shattered. Global oil inventories are now being depleted at what the IEA calls a “record pace”, and with peak summer demand approaching, the agency warned this week that “further price volatility appears likely.”

The economic damage extends far beyond the energy sector. UNCTAD has documented disruptions to methanol, aluminium, sulfur, graphite, and industrial chemicals — commodities underpinning everything from fertiliser production to the green energy transition. Global merchandise trade growth is now projected at just 1.5–2.5% for 2026, down from 4.7% in 2025. The Dallas Fed estimated the closure would reduce annualised global GDP growth by 2.9 percentage points in Q2 2026 alone if sustained.

The Trump-Xi Moment: A Diplomatic Opening

Against this backdrop, the Trump-Xi summit in Beijing carries an urgency that goes beyond the usual theatre of superpower diplomacy.

On Day 75, the White House confirmed a critical development from the first session of talks: both Trump and Chinese President Xi Jinping agreed that the Strait of Hormuz must remain open for the free flow of global energy. Xi also signalled China’s interest in purchasing more American oil — a gesture designed to reduce Beijing’s dependence on Iranian crude and align its commercial interests with a reopened strait.

Oil markets responded with cautious optimism, holding near $105 rather than spiking further — a signal that investors interpreted the Hormuz statement as meaningful, even if not decisive.

The harder ask — whether China will actively pressure Tehran to accept the 14-point memorandum of understanding currently stalled in Iranian review — remained the unanswered question. China buys over 80% of Iran’s exported crude, giving Beijing leverage over Tehran that no other country possesses. If Xi applies that leverage, the economic calculus for Iran shifts dramatically. If he does not, Day 75 becomes Day 100 without a resolution, and the IEA’s warnings about price volatility become self-fulfilling.

$100 Oil and the American Household

For the US stock market, which has climbed to record highs above 7,400 on the S&P 500 partly on peace deal expectations, every day above $100 oil is both a corporate earnings story and a household affordability crisis. Gasoline across the United States averages $4.50 per gallon, up more than $1.50 since February 28. Inflation rose to 3.8% annually in April — its highest in nearly three years — with energy accounting for over 40% of the CPI increase.

The EIA’s May Short-Term Energy Outlook projects that Brent could reach $154 per barrel if the Strait remains closed for 12 weeks — a scenario that, on Day 75, is already past the six-week threshold once considered the outer boundary of the crisis.

Every day the Hormuz chaos continues, the global economy pays a compounding price: in stranded ships, in depleted inventories, in inflated energy bills, in stunted growth, and in the quiet desperation of 20,000 seafarers still waiting to go home.

In Beijing, Day 75 may have produced the first real diplomatic signal that the end is in sight. Whether it translates into oil below $100, reopened shipping lanes, and a deal signed in Tehran — that is the question the market, and the world, is now asking.

Market Analysis

A quick snapshot of market trends, customer behavior, and competitor movements.